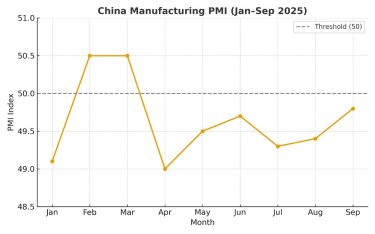

The decline in China’s manufacturing PMI underscores the damage caused by the United States 145 per cent tariffs on Chinese goods. Chinese manufacturers felt the brunt as orders started getting cancelled and output being cut in tandem. In April, Robin Xing, chief China economist at Morgan Stanley, had warned in a research note stating, “We believe the tariff impact will be the most acute this quarter, as many exporters have halted their production and shipments to the US, given heightened tariff uncertainties. The overall policy framework remains reactive and supply-centric, insufficient to offset tariff shocks.”

Scene across the construction and automobile sectors

Within the broader industrial mix, the construction and automobile sectors have charted divergent courses. While one showed a weakening trend, the other stood firm. China’s construction PMI averaged 55.6 points from 2021 until September 2025. It reached an all-time high of 69.10 points in November of 2021 and a record low of 49.10 points in August 2025. In September, the PMI increased marginally to 49.30 points. However, until July 2025, the country’s construction PMI hovered above the threshold of 50 points, standing at 52.70 in February, 53.40 in March, 51.90 in April, 51 in May, 52.80 in June, and 50.60 in July. These data show that even though the monthly PMI stood above the benchmark yet recorded overall drop.

In contrast, the automobile sector has been a rare bright spot. According to the China Association of Automobile Manufacturers (CAAM), the country’s automobile production and sales exceeded 20 million units between January and September 2025 – a record high for the period. In August, the production and sales stood at 2.82 million units and 2.86 million units, which in September increased to 3.276 million units and 3.226 million units, respectively, mirroring the trend seen in March 2025 when output remained high despite softer consumer sentiment. China’s automobile sales in March were 2.92 million units as against the production of 3.01 million units.

Aluminium industry feels the strain and also the support

China’s aluminium sector has historically thrived on the country’s construction and automobile industries. For decades, manufacturers producing components for window frames, door handles, railings, and other architectural elements enjoyed steady growth. So, the contraction in the construction PMI index has impacted the aluminium sector in several ways like - best-performing aluminum processors are now operating at just 60-70 per cent capacity, weeaker companies function at only 40-50 per cent capacity, industry experts consider 80 per cent the minimum threshold for healthy operation, and processing fees have reached historic lows as companies desperately compete for dwindling orders.

In parallel, China’s automobile industry growth has backed the aluminium sector. In September 2025, China’s primary aluminium alloy PMI stood at 59.7 per cent, up by 0.3 percentage points from 59.4 per cent in August. Breaking down the components, both production and new orders index stood stable at 68.6 per cent and 66.7 per cent, respectively. Amid relatively unstable changes in the operating capacity of primary processing sectors like aluminum billet, the production side of primary aluminum alloy continued to exert effort, with order performance being particularly strong, especially the notably substantial export situation for downstream finished products.

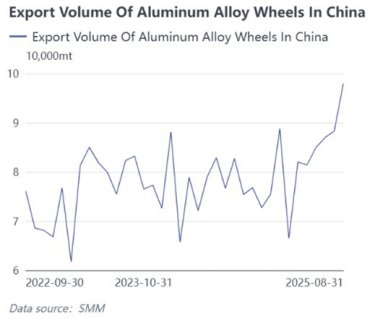

According to SMM, China's aluminum alloy wheel hub exports in August increased significantly by 9,600 tonnes to 97,900 tonnes, up by 10.9 per cent M-o-M and 18.4 per cent Y-o-Y, hitting a three-year high. The finished product inventory index was 43.1 per cent, a noticeable decrease from 53.0 per cent in August, while the purchasing volume index was 59.8 per cent, indicating inventories are in a more reasonable range and procurement activities are relatively active, suggesting enterprises maintain a steady pace in inventory management and raw material procurement.