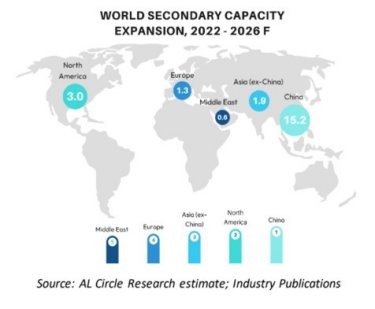

Over the years now, global aluminium recycling market is on the upward trajectory, with recycled aluminium usage standing at 27.7 million tonnes in 2023 and 28.4 million tonnes in 2024, driven by the growing focus on sustainability and circular economy practices. AL Circle’s comprehensive industry focus report, titled: “World Recycled ALuminium Market Analysis Industry Forecast to 2032”, highlights that by the end of 2032, the global aluminium recycling market size is poised to grow at a CAGR of 4.62 per cent from USD 107.05 billion in 2023 to USD 160.8 billion.

Demand forecast in line with usage

What is driving this growth? Certainly, the growing demand for recycled aluminium products. Rusal forecasts the incremental global demand for aluminium is set to reach 17.3 million tonnes by 2029, with recycled aluminium expected to contribute a substantial 69 per cent, compared to 31 per cent from primary aluminium.. In China, the dominance of secondary aluminium will be even stronger, accounting for 84 per cent of the projected 5.3 million tonnes of incremental demand. Overall, the share of recycled aluminium in total metal processing is expected to climb from 30 per cent in 2024 to 36 per cent by 2029.