The world alumina production concluded the third quarter of 2025 with a positive trajectory, overcoming a soft September thanks to strong output in July and August when the volume reached an all-time high. Although primary aluminium production slowed, alumina output remained tightly aligned with consumption trends.

World Alumina Production aligns with Demand Forecast, with a 6% Growth in Q3 2025

Strong momentum keeps alumina output aligned with consumption

According to the International Aluminium Insitute, the world alumina production volume in Q3 2025 amounted to 39.387 million tonnes versus 37.225 million tonnes, reflecting a Q-o-Q rise of 5.81 per cent. While metallurgical-grade climbed up from 34.937 million tonnes to 37.002 million tonnes, chemical-grade grew from 2.288 million tonnes to 2.385 million tonnes.

Through the first nine months, the output also showed a bullish trend, standing at 114.099 million tonnes, to which metallurgical-grade alumina contributed 107.275 million tonnes and chemical-grade accounted for 6.824 million tonnes. Compared this to the previous year, the world total alumina output stood at 108.880 million tonnes, of which metallurgical-grade was 102.241 million tonnes and chemical-grade was 6.639 million tonnes. So, annually, both metallurgical-grade and chemical-grade recorded growth of 4.9 per cent and 2.8 per cent, respectively.

In line with the 107.275 million tonnes of production, consumption stood at 109.7 million tonnes. For the full-year, alumina consumption projection is 142 million tonnes, which is also aligned with the production forecast of around 145 million tonnes.

Drop in September without dampening Q3 output

In September 2025, the world alumina production (including chemical-grade) witnessed a 3 per cent decline, coming in at 12.884 million tonnes. Of this, the output of metallurgical-grade alumina stood at 12.138 million tonnes, while chemical-grade at 748,000 tonnes. They both saw M-o-M plunge of 3 per cent. Behind the monthly decline in September, all the key alumina producers are responsible – from China to Oceania and even Africa & Asia (ex-China).

In China, the output of metallurgical-grade alumina during September was 7.553 million tonnes, down by 1 per cent from 7.629 million tonnes in August, while the production in Oceania and Africa & Asia was 1.391 million tonnes and 1.185 million tonnes versus 1.456 million tonnes and 1.266 million tonnes, reflecting declines of 4.5 per cent and 6.4 per cent.

The drop in China’s monthly alumina production could be attributed to “September 3rd military parade" event, when some alumina refineries in the north periodically reduced the load of roasting furnaces.Simultaneously, some enterprises in the south conducted planned routine maintenance, which also reduced the roasting load. Additionally, bearish alumina prices narrowed corporate profit margins, leading to low enthusiasm for production increases.

South America also mirrored the trend and recorded M-o-M fall of 10 per cent to 905,000 tonnes. Although all the producers witnessed declines, but among them all South America saw the steepest fall, followed by Africa & Asia (ex-China), Oceania, and then China.

Q3 production reinforces market resilience, except in Europe

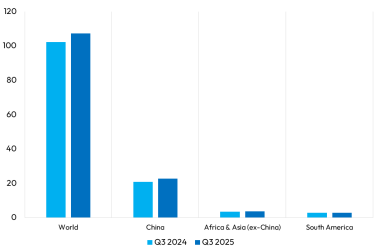

However, despite the monthly declines, none of these regions saw a fall over the quarter in Q3 2025. For instance, in South America, the production of alumina was 2.846 million tonnes, up by 3.6 per cent from 2.748 million tonnes in Q2 2025. Even over the year, the output recorded an increase of 2.78 per cent from 2.769 million tonnes. During the same period, Africa & Asia (ex-China) witnessed a sequential growth of 2.93 per cent in alumina production from 3.586 million tonnes to 3.691 million tonnes, and over the year by 6.7 per cent from 3.46 million tonnes.

In China, the world’s largest alumina producer, the output stood at 22.76 million tonnes during the third quarter of 2025, up by 8.2 per cent Q-o-Q from 21.043 million tonnes and 8.85 per cent higher than 20.91 million tonnes.

Compared to these regions, Europe (including Russia) experienced relatively muted growth of only 0.4 per cent from 1.420 million tonnes to 1.425 million tonnes. Annually, on the other hand, the production volume recorded a plunge of 6 per cent from 1.515 million tonnes. This scenario could be attributed to the challenges faced by Europe’s largest alumina refinery named Aughinish Alumina, which in July 2025 was suspended from Ireland’s ex-ante energy market, meaning it is prohibited from participating in future energy trading. This challenge adds to the refinery’s age-old raw material supply issue since March 2022, when Rio Tinto stopped supplying bauxite as a result of geopolitical tensions.

Conclusion: Strong fundamentals despite short-term volatility

While September introduced a brief setback, the overall growth in alumina production during Q3 2025 showcased robust fundamentals supported by tight alignment with consumption and resilient output across major regions. Temporary operational or market-induced disruptions failed to derail the quarterly trajectory, keeping the industry on track for a stable full-year performance.

Source:AL Circle