Market research collated in early 2025 places the global aluminium scrap processing pipeline at roughly 38 million tonnes in 2024, with forecasts pointing to about 57 million tonnes by 2030 (a 7 per cent CAGR from 2024–2030). That projection is built on expected growth in automotive, packaging and building applications and on investments in sorting and remelting technologies.

Can the Recycling Industry Scale for the 2030 Goals? We Ready to Shift to an All-Aluminium Recycling World?

For context at the national level, U.S. Geological Survey Publications states that in the United States, recovered aluminium from purchased scrap in 2024 was about 3.27 million tonnes, of which new (manufacturing) scrap accounted for roughly 56 per cent and old (post-consumer) scrap roughly 44 per cent; old-scrap recovery equated to about 37 per cent of apparent domestic consumption.

According to the International Aluminium Institute (IAI), global secondary (recycled) aluminium production in 2024 is estimated at around 33-34 million tonnes, accounting for roughly 35 per cent of total aluminium supply. The number has been steadily rising as more post-consumer scrap becomes available and primary producers optimise closed-loop production cycles.

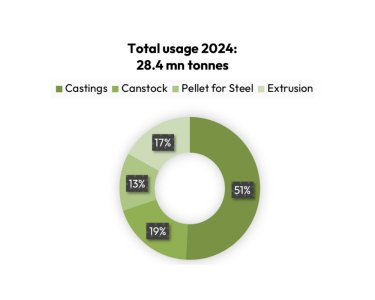

By 2030, IAI and CRU Analytics project recycled aluminium supply could reach 42-45 million tonnes, helped by growth of end-of-life volumes from automotive and construction sectors, increasing OEM recycled-content targets, and regional incentives for low-carbon material footprints. AL Circle estimates 28.4 million tonnes of recycled aluminium to have been used in 2024 in various end-use segments like casting, canstock, pellet for steel and extrusion among others. With stringent laws spreading like fire across the globe, recycling has become not only a mandate but a survival strategy for most industry stakeholders.

The recently held session of the International Trade Council highlighted the central contradiction that aluminium and other metals are now caught in: the desire to secure domestic manufacturing strength versus the need to maintain open access to recycled material flows across borders.

While the panel focused heavily on steel, the underlying dynamics apply almost one-to-one to aluminium as recycled content continues to climb in value across value chains, especially in transport, construction, packaging and electrical applications.

The global aluminium system is shifting from a one-way funnel of primary metal toward a far more circular model. But rising scrap volumes, tightening primary supplies and a tangle of trade and policy brakes mean the outcome is not automatic. Below, I answer five pressing questions the industry might seek answers for.

Is all aluminium scrap apt for recycling?

According to an article by Science Direct, aluminium is nominally infinitely recyclable, but not all scrap is equally usable without extra processing. Several concrete limitations determine whether scrap can be converted cost-effectively into secondary metal:

Post-consumer (old) scrap frequently contains mixed alloys, coatings (paints, lacquers), plastics, and non-aluminium inclusions; these impurities increase the sorting and re-alloying cost and sometimes render the scrap unsuitable for high-value end uses unless upgraded. Academic analysis has quantified that a measurable chunk of scrap will remain technically or economically unrecycled. Researchers estimate that millions of tonnes (on the order of 6.1 million tonnes by 2030 in some projections) may not be recycled because of alloy concentration and contamination constraints unless collection and sorting change materially.

High-performance markets (certain automotive and aerospace alloys) require strict chemistry and low impurities; low-grade recovered metal must be blended, refined or downgraded, adding cost and sometimes defeating the carbon-cost advantage.

Even where scrap is physically recyclable, weak collection systems, long transport distances, along with energy and permit costs, can make recycling unviable locally, and material may be exported to regions with cheaper processing or simply stockpiled.

Thus, while aluminium’s metallurgical recyclability is excellent, the practical recyclability of the scrap stream depends on its grade, contamination level, available sorting technology, and the economics of remelting.

If primary aluminium production deflates and scrap demand inflates, what is going to happen?

A structural shift toward scrap without parallel investment in high-quality scrap processing risks producing a quality gap.

Demand for auto-body sheet, extrusion billet, and aerospace plate cannot be met with contaminated scrap streams. Alongside, if primary capacity contracts too sharply (due to carbon costs or energy constraints), premium-grade rolling and extrusion alloys could tighten.

This would increase price spreads between clean segregated scrap, mixed scrap and primary aluminium (P1020 and billet).

In short, scrap demand rising is good, but only if alloy-correction and remelt capacity expand with it. Otherwise, markets face imbalances, and recycled aluminium cannot fully replace primary aluminium.

What are the speedbreakers that may hinder the path for recycling in aluminium?

Tariffs that protect domestic primary smelters can raise domestic metal prices and lead recyclers to lobby for preferential treatment. At the RECYCLING magazine session at the BIR World Recycling Convention in October 2025, industry leaders flagged that tariff measures create more bureaucracy, redirect trade flows and can reduce incentives for efficient recycling-led supply. Some US recyclers have openly supported tariffs to protect domestic processing. Such measures change scrap-to-metal arbitrage and can raise domestic production costs.

The EU Carbon Border Adjustment Mechanism (CBAM) is raising import costs for carbon-intensive aluminium, but also increasing compliance workloads for recyclers. Calls inside the EU to restrict exports of scrap are growing, based on the belief that keeping scrap inside Europe will strengthen local manufacturing.

Emmanuel Katrakis of Galloo countered this directly at the ITC, “Whenever consumption rises, scrap exports fall. The market regulates itself.” His data showed EU recycled metals consumption has fallen by 10 million tonnes in a decade due to lower industrial output, not lack of scrap availability.

High industrial electricity prices (as flagged by European recyclers) and slow permitting for expansion blunt the competitiveness of secondary smelters in high-cost jurisdictions. In many cases, energy cost is the decisive factor that makes recycling profitable or not.

And, accusations of subsidised foreign production can prompt anti-dumping duties or safeguards that reshape imports of both primary and recycled metal. Those measures add uncertainty to long-term capital planning.

Emmanuel Katrakis of Galloo countered this directly at the ITC, “Whenever consumption rises, scrap exports fall. The market regulates itself.” His data showed EU recycled metals consumption has fallen by 10 million tonnes in a decade due to lower industrial output, not lack of scrap availability.

This is where the ITC debate becomes central. For the United States, Section 232 tariffs continue to protect domestic mills.

George Adams of SA Recycling has argued, “Tariffs are single-handedly saving our steel industry… I want more mills, so they pay more for scrap.” However, US recyclers pushed back hard in 2025 against proposals to restrict aluminium and copper scrap exports. ReMA’s 2024–2025 market availability study found no evidence of domestic scrap shortages.

In Asia, China has shifted production to Thailand and Southeast Asia to avoid tariff friction. As Mark Sellier noted, US scrap exports to Canada rose by 30 per cent when tariffs began, and Canadian exports to China grew by a similar margin. The material flowed anyway; it just took a longer route.

What about facility expansion? Are we ready for the future of the aluminium recycling market?

Readiness is uneven and measurable. Two sets of facts make this clear, one is where the industry is investing. Market reports and vendor activity show significant investment in sorting (LIBS, sensor-based separation), automated baling, and secondary remelt capabilities. Regions with existing downstream manufacturing (notably parts of Asia-Pacific) are expanding capacity to capture growing scrap volumes and to feed automotive and packaging demand. Research-and-market forecasts that underpin the 2024 to 2030 volume projections also assume considerable capital deployment into sorting and remelting lines. And the other where the gap remains.

Several hard data points show capacity and structural shortfalls:

• In the US in 2024, secondary production (from new and old scrap) remained essentially unchanged from recent years, even as primary production shifted, signalling that secondary capacity is not scaling in lockstep with market signals. That stagnation is a red flag when global scrap volumes are projected to rise sharply.

• Quality constraints and the academic projection that several million tonnes of scrap may remain unrecycled unless sorting and collection improve point to an operational readiness gap. Scaling will not be just more furnaces; it will require better front-end systems (collection, segregation, decoating) and upgraded remelt/refine capability.

• Policy uncertainty is slowing some investments. Where governments signal possible export levies, tariffs or CBAM changes, investors hesitate or re-route capital to jurisdictions with clearer or more favourable frameworks. That creates regional mismatches: places with feedstock but no processing, and places with processing capacity but no secure access to low-carbon scrap feedstock.

Source:AL Circle