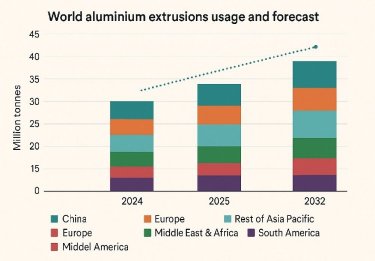

As 2025 draws to a close, the aluminium extrusion industry finds itself steadier than it started, as global usage is expected to settle at 35.25 million tonnes, just above 34.27 million tonnes in 2024, a modest 2.8 per cent increase that reflects stability in a market still navigating post-pandemic aftershocks. The pressures haven’t eased: geopolitical tensions continue to shift unpredictably, construction activity remains slower than before 2020, major economies struggle to regain momentum, and energy costs stay elevated.

Yet the longer arc remains upward. Forecasts suggest the sector could reach 43.58 million tonnes by 2032, supported by a 3.05 per cent CAGR. By the end of 2025, the defining theme is clear—not a dramatic rebound, but a steady, resilient climb.

If 2024 proved anything, it’s that China’s grip on the aluminium extrusion market is as firm as ever. The country accounted for around 65 per cent of global usage that year — an extraordinary share by any measure. Europe follows next, then the Rest of Asia Pacific, and after that North America with just 8 per cent, and the Middle East & Africa with 4 per cent.

China continues to pull further ahead in 2025, lifting its aluminium extrusion consumption from 22.32 million tonnes in 2024 to roughly 22.87 million tonnes, and the outlook suggests it will keep expanding at about 3.16 per cent a year through 2032. The Rest of Asia Pacific is on an upward track as well, moving from 3.16 million tonnes to 3.31 million tonnes, supported by a stronger 3.62 per cent CAGR.

North America’s growth is more modest but consistent, rising from 2.86 million tonnes in 2024 to around 2.93 million tonnes, in line with its 2.29 per cent CAGR. South America also moves ahead, increasing from 0.86 million tonnes to 0.90 million tonnes, backed by a 3.24 per cent CAGR.

Europe shows only a slight change—3.43 million tonnes in 2024 edging up to 3.49 million tonnes—which makes it the slowest-growing region with a 1.91 per cent CAGR. In contrast, the Middle East & Africa records the strongest momentum, rising from 1.64 million tonnes to 1.75 million tonnes, and leading the global growth outlook with a projected 3.84 per cent CAGR through 2032.

Recovery and realignment

The memory of the last ten years remains fresh. Until 2019, the market expanded with rhythm. Then 2020 broke that rhythm entirely. Lockdowns silenced factories, paused construction, and halted demand almost overnight. Yet 2021 surprised many by bouncing back sharply—so sharply, in fact, that it restored pre-pandemic consumption levels.

As 2025 unfolds, the effects of that disruption continue to ripple. Building and construction, long the industry’s anchor, is finally letting out some of the pent-up demand accumulated over years of delays. Meanwhile, the global appetite for electric and lightweight vehicles keeps reshaping production lines everywhere. And in the background, another giant quietly grows: data centres.

Their electricity needs are climbing so fast—in the United States, China and the Middle East especially—that power producers are accelerating solar PV installations. Clean-energy infrastructure, from frames to mounting systems, is pulling aluminium extrusions with it.

North America: A market pulled by roads and buildings

North America’s extrusion market feels grounded, not explosive. Transport applications used 924,000 tonnes in 2024, and by 2032 that figure is forecast to reach 1.19 million tonnes, carried by 3.21 per cent annual growth. Passenger cars and light commercial vehicles still take 30–40 per cent of the volume; trailers and semi-trailers follow. The aluminium inside these vehicles is climbing too—from 45 pounds per vehicle in 2020 to an expected 95 pounds by 2032.

The region’s buildings are also changing shape. Multi-glazed façades, full-glass doors, reversible window systems, impact-resistant frames — all of them lean heavily on aluminium. Although UPVC and steel sometimes cut in, extrusions maintain momentum, with construction use expected to reach 970,000 tonnes by 2032.

Electrical and electronics consumption stands near 273,000 tonnes in 2024 and should approach 309,000 tonnes by 2032. Industrial usage grows more sharply, from 380,000 tonnes to 509,000 tonnes.

South America: A region building its way forward

South America used 860,000 tonnes in 2024 and is on its way toward 1.11 million tonnes in 2032. Brazil, unsurprisingly, sets the tone, with 55 per cent of total regional consumption. Building and construction is the region’s biggest pull: 413,000 tonnes in 2024, projected to grow to 543,000 tonnes by 2032, supported by a 3.49 per cent CAGR and years of ongoing infrastructure investment.

Europe: growth hidden beneath layers of strain

Europe’s relationship with aluminium extrusions is shifting. Transport accounted for about 950,000 tonnes in 2024, rising to 1.2 million tonnes by 2032. Electric-vehicle development is changing design priorities, bringing extrusions into battery

enclosures, charging-station structures and motor housings. Curiously, average extrusion content per light vehicle is falling—from 27 kg in 2022 to a forecast 19.5 kg by 2032—as manufacturers chase efficiency in every component.

On the production front, lightweight commercial vehicle output slipped to 2.09 million units in 2024, down 5.8 per cent, while EU-27 and UK production together dropped to 1.54 million units, a 7.24 per cent fall from 2023.

Construction numbers tell a similar story of uneven footing. EU construction output in May 2025 dropped 1.3 per cent month-on-month; the euro area declined 1.7 per cent. Yet year-on-year comparisons show increases of 2.7 per cent and 2.9 per cent in EU and UK respectively. After a 2 per cent contraction in 2024, forecasts suggest a measured rebound: 1.1 per cent growth in 2025 and 0.8 per cent in 2026. In the UK, the December 2024 Construction PMI slipped to 53.3, its lowest in half a year, but still signals expansion.

China: Several markets packed into one country

China’s extrusion story stretches across multiple sectors. Transport alone consumed 3.68 million tonnes in 2024, heading toward 5.69 million tonnes by 2032. The first eight months of 2025 were especially strong: more than 20 million vehicles were produced and sold, that created an extrusion product demand.

NEVs were the standout. Between January and August, 9.6 million NEVs were sold—a 35 per cent jump—capturing 45–50 per cent of all vehicle sales and more than doubling export volumes.

Industrial and electronics usage remains heavy too: 1.47 million tonnes and 2.43 million tonnes, respectively, in 2024. China also remains the world’s biggest solar component manufacturer.

Trade conditions were tougher. After exporting 916 kt in 2023, momentum cooled in 2024. Early-2025 exports of unwrought and semi-finished aluminium reached 859 kt (Jan–Feb), down 11 per cent year-on-year. February’s 408 kt marked drops of 9.5 per cent month-to-month and 12.7 per cent year-to-year as anti-dumping rules and tariff risks complicated flows, including indirect routes through third countries.

Construction remains China’s biggest extrusion user—57 per cent of the total in 2024 — but that share is expected to fall to 51 per cent by 2032 as transport, electronics and renewable-energy usage accelerate faster.

Rest of Asia Pacific: Construction at the core

Construction anchors the ROAP region, accounting for about 54 per cent of all extrusion consumption. Transport demand, sitting at 515,000 tonnes in 2024, should reach 752,000 tonnes by 2032, with 4.84 per cent CAGR growth led by India, South Korea and Southeast Asia. Construction, at 1.7 million tonnes in 2024, heads toward 2.2 million tonnes by 2032, backed by 3.19 per cent CAGR.

Japan’s usage sits near 354,000 tonnes in 2024; while its growth is slower, emerging markets around it are driving regional momentum.

Middle East & Africa: Quiet growth, clear direction

In the Middle East & Africa, extrusion demand reached 1.64 million tonnes in 2024. By 2032, it is expected to move past 2.22 million tonnes, supported by a 3.84 per cent CAGR. Construction dominates with 1.35 million tonnes in 2024 and a path to 1.80 million tonnes in 2032, moving at 3.63per cent CAGR.

Transport grows from 61,000 tonnes in 2023 to 95,000 tonnes in 2030. Electrical and electronics usage increases from 60,000 tonnes (2024) to 75,000 tonnes (2032). Industrial demand grows from 100,000 tonnes to 152,000 tonnes, driven by a strong 5.37 per cent CAGR.

Source:AL Circle