Aluminium foil is no longer used solely in conventional sectors such as food packaging or air conditioning. Its role has expanded dramatically into high-tech, high-growth industries that are central to China’s industrial policy. These include:

• Electric vehicles (EVs) and lithium-ion batteries

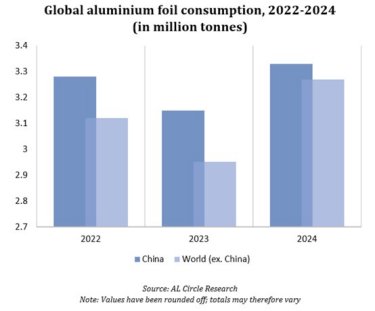

The most significant new driver of foil consumption is battery production. Aluminium foil is used as the positive current collector in lithium-ion batteries. With China leading global EV production (accounting for more than 60 per cent of global sales in 2023), battery-grade aluminium foil has become a strategic commodity. Each GWh of battery production consumes up to 800 tonnes of foil. Leading battery producers have significantly scaled up their capacity, and this trend is expected to continue even as broader economic indicators slow. Importantly, this demand is policy-insulated—backed by subsidies, R&D incentives, and green mandates from the Chinese government.

• Energy storage systems (ESS)

The rise of renewable energy and grid stability projects across China has led to a parallel boom in energy storage systems. These also require lithium-based batteries—therefore increasing demand for foil. Unlike the consumer-driven EV segment, ESS demand is tied to state investment in energy transition, which remains robust despite the macroeconomic environment.

• Pharmaceutical and medical packaging

Aluminium foil remains indispensable in drug blister packs, medical pouches, and sterile packaging. Although not as fast-growing as EV applications, the pharmaceutical sector has become more prominent since the COVID-19 pandemic. China is scaling up domestic pharmaceutical production, not only for domestic consumption but also for export. This creates stable, resilient demand for high-barrier, contamination-resistant foil products.

• Food packaging and E-commerce logistics

While broader consumer demand may be soft, e-commerce and online food delivery continue to grow, albeit at a slower rate. Aluminium foil-based multilayer packaging—used for insulation, hygiene, and shelf-life extension—remains a key material in these supply chains. China's increasing preference for sustainable and recyclable packaging also favours aluminium over plastic.

• Consumer electronics and semiconductors

Another advanced use case lies in thermal management solutions for electronics—cooling devices, smartphone batteries, and chip packaging. China's ambitions to achieve semiconductor self-reliance are still nascent but already spurring upstream demand for speciality materials, including aluminium foil for heat sinks and precision components.

Moreover, the nature of aluminium foil demand is increasingly quality-sensitive. Ultra-thin, high-purity foil for batteries and electronics is replacing the bulk consumption of conventional packaging foil. This technological upgrade is driving value growth even when volume growth is modest.

Looking for insights into the fast-evolving aluminium flat rolled products market? "Aluminium Flat Rolled Products: Insights & Forecast to 2030" covers global trends, grade-wise demand (1XXX, 3XXX, 5XXX), and key end-use sectors. From regional shifts to industrial drivers, it’s your roadmap to understanding this vital industry.

In essence, aluminium foil demand in China is a microcosm of China's economic rebalancing: slower in speed, sharper in focus, and deeper in strategic alignment with national goals. Despite macro headwinds, aluminium foil has become embedded in the material's backbone of the industries China is doubling down on.

Aluminium foil demand in the Rest of the Asia Pacific region, which includes Japan along with key emerging economies such as India, South Korea, Thailand and Indonesia, is expected to grow at an average annual rate of approximately 4.17 per cent between 2024 and 2030. Within the region, India is projected to experience relatively stronger growth, with aluminium foil consumption expected to increase at around 5.4 per cent per annum over the same period.

Source:AlCircle