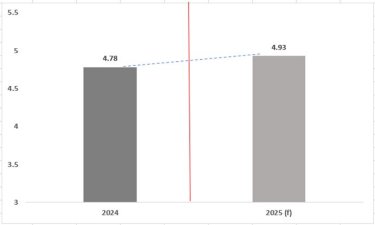

The global aluminium industry stands at a critical juncture where efficiency, sustainability, and resource recovery are shaping new business priorities. As per recent business market research, the aluminium sector — formed of primary aluminium smelters, secondary aluminium facilities, and downstream processing plants — generated an estimated 4.78 million tonnes of dross in 2024.

This figure reflects the inescapable byproduct of aluminium melting, but it also highlights opportunities for resource recovery and value creation.

Aluminium dross generation: Regional market analysis

China, the world's largest producer of aluminium, continues to dominate global dross output as per rule, accounting for nearly 47 per cent of total generation in 2024. The Rest of Asia-Pacific (excluding China), Europe, and North America followed as other significant contributors. As a result, the geographical spread emphasises the fact that aluminium dross generation closely mirrors aluminium production and recycling capacities across these regions.

Notably, the secondary aluminium sector was responsible for generating over half of the world’s dross in 2024, reflecting the sector’s increasing importance in global aluminium supply chains. Meanwhile, primary aluminium producing smelters accounted for around 18 per cent, with the balance arising from downstream processors with their own melting facilities.

Dross characteristics and processing trends

Dross generation varies depending on factors such as furnace type, feedstock quality, and operational practices. On average, 0.8 per cent–1.5 per cent of primary aluminium output results in dross, while recycled aluminium typically yields around 7 per cent dross due to the higher presence of coatings, impurities, and oxide formation.

In terms of type, black dross accounted for 73 per cent of global generation, while white dross made up the remainder. The two forms of aluminium dross generated vary not just in appearance but also in aluminium content, like white dross contains between 40 per cent - 80 per cent aluminium, while black dross averages only 5 per cent - 25 per cent. This significant variation in recoverable metal content directly influences both processing strategies and commercial outcomes.

Across the industry, companies are investing in improved dross management. Many facilities now process dross onsite to maximise aluminium recovery, while others collaborate with specialised third-party processors. This shift reflects a broader global market trend towards minimising waste, maximising resource efficiency, and aligning operations with environmental, social, and governance (ESG) standards.

Aluminium recovery and economic impact

Of the 4.78 million tonnes of dross produced globally in 2024, an estimated 1.12 million tonnes of aluminium metal were recovered. Although impressive, this figure suggests untapped opportunities for higher recovery rates. For instance, in processing routes where salt is added, the resulting salt slag still contains 3 per cent – 6 per cent aluminium, indicating scope for technology innovation and secondary recovery solutions.

The commercial implications are significant. Recovered aluminium metal not only reduces raw material dependence but also supports cost competitiveness in an industry sensitive to energy and commodity price fluctuations. For many operators, dross recovery has become a profit centre as much as a sustainability initiative.

Forecast for 2025: Rising volumes, rising responsibilities

As per AL Circle Research's estimate, global dross generation is forecasted to reach 4.93 million tonnes in 2025. However, this increase will be driven by rising recycling of aluminium in capacity and volumes and expanding downstream consumption, and the dross recycling report unveils sector-wise classification.

Aluminium dross generations: 2024 - 2025 (f) (in million tonnes)