Why aluminium alloy prices are higher in 2025 vs 2024?

Aluminium alloy LME prices began 2025 on stronger ground, marking a shift upward from the levels seen a year earlier. The LME offer price opened in January at around USD 2250 per tonne but quickly slipped to approx. USD 2100 per tonne.

For much of the first quarter, values held between USD 2100 and USD 2500 per tonne. From March 17, momentum turned higher, reaching USD 2547 per tonne and closing the month at USD 2577 per tonne.

This was tied to developments in US trade policy. In February, Washington lifted aluminium tariffs under Section 232 from 10 to 25 per cent, effective March 12, 2025, while scrapping exemptions. Buyers rushed to secure supplies before the higher duties came into effect, boosting inventories and advancing shipments. Some attempted to claim exemptions for “melted and poured” U.-origin aluminium, though these required complex documentation.

April brought a reversal. Prices slipped from USD 2575 per tonne at the start of the month to USD 2455 per tonne on April 9 and USD 2402 per tonne on April 10. They then recovered to USD 2509 per tonne on April 14, a level that held steady through September 15.

Bid prices traced the same path, beginning at around USD 2250 per tonne, dipping to approx. USD 2100, rallying in March to around USD 2577 per tonne, and then flattening at USD 2499 from mid-April through September.

The comparison with 2024 is striking. That year began with prices near USD 1800 per tonne. They climbed to USD 2200 per tonne, peaked at USD 2767.8 per tonne in August, and corrected to about USD 2300 per tonne by September. Bid values moved in the same arc. Unlike that pattern, 2025 started higher and, after an early rise, steadied around USD 2500 per tonne.

Global consumption outlook

The firmer base in 2025 reflects stronger consumption. According to FMI, global demand for aluminium alloys this year is expected to range between USD 155.1 billion and USD 167.3 billion. The main sectors driving growth are transport, automotive, construction and infrastructure.

Automakers are stepping up their use of alloys to cut weight and meet efficiency and emissions standards. India and China continue to support demand through large-scale construction and infrastructure work. Aerospace also plays a role, with manufacturers relying on high-strength grades to reduce aircraft weight.

Still, the growth picture has been uneven. Until June, consumption was relatively muted. In the US and Europe, tariffs raised costs, and several processors and auto parts makers scaled back or paused output. Europe’s supply base remains constrained, with almost half of its smelting capacity offline since 2023 due to high energy prices.

Tariffs now cover not just raw metal but aluminium-containing parts such as axles, brackets and chassis components. That has complicated sourcing for suppliers and led to production cuts. Stellantis facilities in Canada and Mexico reported disruptions, while luxury carmakers such as Audi and Jaguar Land Rover temporarily halted shipments to the US before adjustments were reached.

The aerospace sector faces its own challenges. Boeing and Airbus are dealing with billions in extra costs as tariffs rose to as high as 50 per cent, delaying programme schedules. Consumer goods are also affected, with duties extending to appliances, packaging and electronics. The US beer industry alone faces higher costs on more than USD 6 billion worth of imported cans from Mexico.

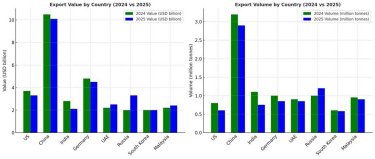

Export movements across key markets

Trade flows show the strain on supply chains. US exports fell from USD 3.6 billion and 804,672 tonnes in June 2024 to USD 3.2 billion and 562,175 tonnes in June 2025.

China held its lead as the world’s largest exporter but saw shipments dip from 3.16 million tonnes worth USD 10.4 billion to 2.9 million tonnes worth USD 10.1 billion. Its position is dominant but is under pressure. The government scrapped aluminium export tax rebates in December 2024, a move expected to trim shipments by 8–11 per cent in 2025 as supply is directed to domestic use. Production limits at about 45 million tonnes add another brake.

With trade barriers in the US and EU closing off key markets, Chinese exporters have shifted toward Southeast Asia. Exports were strong early in the year as firms shipped ahead of tariff changes but slowed by mid-year as inventories evened out.

India’s exports declined from USD 2.8 billion and 1.15 million tonnes in May 2024 to USD 2.2 billion and 757,832 tonnes a year later. Germany’s volumes fell as well, from USD 4.7 billion and 1 million tonnes to USD 4.4 billion and 889,810 tonnes, reflecting Europe’s energy and logistics difficulties.

Some producers moved the other way. The UAE increased exports from USD 2.2 billion in April 2024 to USD 2.5 billion in April 2025, despite a slight dip in tonnage. Russia posted a stronger jump, from USD 2.3 billion and 966,869 tonnes to USD 3.3 billion and 1.2 million tonnes.

South Korea and Malaysia recorded smaller but steady gains. South Korea rose from USD 1.97 billion and 570,644 tonnes in 2024 to USD 2.1 billion and 588,154 tonnes in 2025. Malaysia increased exports from USD 2.2 billion and 944,604 tonnes in May 2024 to USD 2.4 billion and 903,081 tonnes in May 2025.

Policy drivers and export declines

The shift in trade patterns from 2024 to 2025 has been shaped by policy and supply factors. In June, the US doubled tariffs on steel and aluminium imports from 25 to 50 per cent under Section 232 of the Trade Expansion Act. The measure applies to the metal content of imports and now covers downstream products such as machinery, appliances and vehicle parts.

The change pushed up costs and cut US purchases by more than a quarter. At the same time, domestic demand in both the US and India absorbed more supply for autos, aerospace and infrastructure, leaving less available for export. Europe struggled with high power prices and logistical bottlenecks, with almost half of its smelting capacity already shut since 2023.

Producers with fewer constraints, notably Russia and the UAE, expanded exports and captured greater global share, filling part of the gap left by others.

Together, the tariff shock, shifting demand and supply constraints have reshaped global trade flows, leaving the aluminium alloy market in 2025 marked by higher prices, uneven growth and a clear redistribution of export power.

Source:AL Circle